Greece is experiencing a paradox that is difficult to find in any other European economy: banks are showing strong profitability, high capital adequacy and improved liquidity, while at the same time thousands of borrowers, households and businesses, are in financial suffocation. The banking system has stabilized, but society has not. And this gap cannot continue.

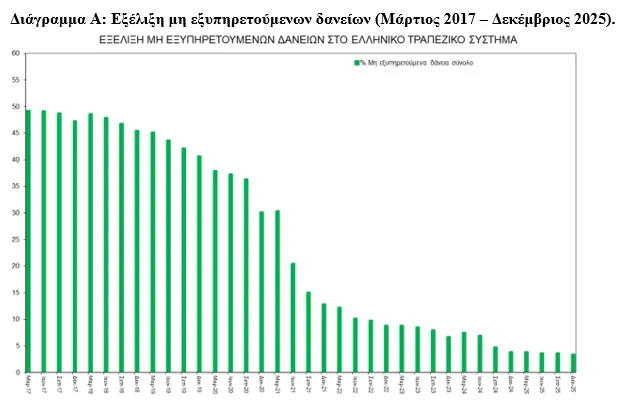

Non-performing loans have decreased dramatically in recent years, but this reduction is more accounting than substantive. The problem has not disappeared; it has simply been transferred. A large part of the "red" loans has passed to debt management companies (servicers), which now hold the fate of tens of thousands of borrowers in their hands. Banks have cleaned up their balance sheets, but borrowers have not cleaned up their problems.

And here is the crux: the majority of those in arrears today are not strategic defaulters. They are people who have been hit by successive crises, a pandemic, an energy shock, inflation, and businesses that remain operationally healthy but financially stressed. Inability to pay is not a choice, it is a consequence.

Despite the spectacular reduction in the non-performing loan ratio to levels approaching the European average, the reality is relentless: the problem remains alive and threatens to resurface. Servicers operate on the basis of recovery, not sustainability. Regulations are often rigid, standardized, and disconnected from the real capabilities of borrowers. And the pressures are increasing.

Greece cannot afford a new generation of “red” loans. It cannot afford to lose productive units that can be saved. It cannot afford to drive thousands of households into economic and social marginalization. The management of arrears is not a technical issue, it is a matter of social cohesion and economic strategy.

International experience is clear: when viable businesses are saved, jobs, investments and tax revenues are saved. When households are supported, consumption and social stability are strengthened. On the contrary, aggressive recovery leads to economic contraction and social tension.

This is why a new, bolder and fairer strategy is required:

- Adjustments based on sustainability, not the accounting picture. Solutions must be adapted to the real capabilities of the borrower. No horizontal regulations, no “copy paste” proposals.

- Substantial restructuring for businesses. Lengthening the duration, reducing burdens, combined solutions that allow the survival of production units. The economy cannot afford to lose businesses that can be saved.

- Strict supervision of servicers. The state must ensure that fair practices are applied and that borrowers have access to transparent procedures. Their operation cannot be uncontrolled.4. Protection of non-strategic defaulters.

- Borrowers affected by exogenous crises must be treated with social sensitivity and not as a “risk to be liquidated”.

- Co-financing mechanisms for viable businesses. State-bank cooperation can reduce risk and allow businesses worth saving to be saved.

- Strengthening financial literacy. Borrowers must be able to evaluate their options and negotiate effectively.

Greece cannot talk about development as long as a large part of society remains trapped in arrears of loans with no prospects. The problem of non-performing loans is not an accounting exercise. It is a matter of justice, sustainability and economic prospects.

And the time for solutions is not tomorrow. It is now, before the problem returns bigger than ever.

*Nikolas Georgikopoulos is a visiting Research Professor of Finance (Stern Business School - NYU) - Chairman of a committee at the Hellenic Development Bank - Scientific Advisor for Development & Investments of the Municipality of Penteli.